I had the pleasure to interview Felix Gode of Alpha Star Funds. Here you can find the full video of the interview and the transcript. This conversation is also available on the Good Investing Talks Podcast.

By loading the video, you agree to YouTube’s privacy policy.

Learn more

- Introduction

- Investing in German-speaking countries

- Things learned in 2020-2021

- What things changed in the process over the last 5 years, Felix Gode?

- The two phases of Alpha Star

- Historical returns

- Principles used in building the fund

- Client Structure Changes

- Skin in the game

- Two Strategies for trading

- The universe of companies that Alpha Star has invested in

- How to avoid companies that play dirty

- Portfolio principles of Felix Gode

- Selling companies

- The 5/10/40 rule in portfolio construction

- What's special about Endor, Felix Gode?

- Founder-led companies

- What's special about IVU?

- Playing the long-term game

- Best way to find stocks

- Apply to Good Investing Plus

- Where will Alpha Star be in 5 years, Felix Gode?

- Management evaluation

- Outro

- Disclaimer

Introduction

[00:00:00] Tilman Versch: Hello, Felix. It’s great to have you on. How are you doing?

[00:00:03] Felix Gode: Thank you, Tilman. Thank you for having me today. I’m very excited to be on your show, on your podcast today. It’s my first interview or my first talk in English at all. So, I’m really excited.

[00:00:24] Tilman Versch: I’m looking forward to it and to learn more from you about the German stock market. You’re really an expert there. And I especially bought a cup for you. It’s a fun fact about Germany. I hope you can read it.

[00:00:36] Felix Gode: Fun facts about Germany. No fun in Germany. Go back to work.

[00:00:43] Tilman Versch: Is this true, we Germans are so focused on work?

[00:00:46] Felix Gode: No, I don’t think. This is a stereotype. You should generalize that. I don’t think so. No.

[00:00:56] Tilman Versch: I got this cup from Toby from Shopify. He founded this company in Canada. I saw it on Twitter and had to get it as well.

[00:01:05] Felix Gode: Okay. Cool

[00:01:06] Tilman Versch: It’s quite nice.

Investing in German-speaking countries

[00:01:24] Tilman Versch: How much fun is it to invest in German speaking countries?

[00:01:31] Felix Gode: Well, for me, it’s a hell of a lot of fun. I mean, I am doing this for 18 years now. I’ve never done anything else in my life or in my career but focusing on the German-speaking stock market. Especially, the small and mid-cap markets.

I mean, I am doing this for 18 years now. I’ve never done anything else in my life or in my career but focusing on the German-speaking stock market. Especially, the small and mid-cap markets.

For me, this is as much fun today as it was 18 years ago. This is a field that is never getting boring. There’s so much to learn, so much to experience, so many new things to learn.

I mean, after 18 years, focusing on this segment, you might think that there’s nothing new to come, but there are a lot of things that are new every day, every week. So, it’s not getting boring at all.

Things learned in 2020-2021

[00:02:28] Tilman Versch: What new things are you learning in 2020 and 2021?

[00:02:32] Felix Gode: If you look at the stock markets and economy and all the things that happened around Covid-19, certainly, nobody of us has ever experienced something like that before. More things like that or comparable to that in the outcome will happen in the future, but we can’t tell today. So, we have to be curious and have to see what the future will bring.

What I actually mean is not by the market itself, but if you’re analyzing balance sheets or stocks in general or companies, at some point in time you might think, “Okay, I’ve seen everything. I know how to analyze balance sheets. I know how to read them. I know how to use the accounting standards, but there’s always something new that comes up that you can discover.”

And then, you think about it, and you can incorporate it in all your R&D analysis process and that changes a little bit. And so, it’s the way of analyzing how companies emerge and evolve. The way we are looking at companies today is much different than five years ago or 10 years ago. It’s a constant process that is developing over time.

What things changed in the process over the last 5 years, Felix Gode?

[00:04:12] Tilman Versch: What changed in your process over the last five or 10 years?

[00:04:17] Felix Gode: There are so many things. This would be a video on its own, actually. But just to mention a few things, let me think about a couple of things that we are doing differently than five years or 10 years ago.

Over time, what has developed quite significantly is the metrics we are looking at. Ten years ago, in the quite early stage of our company, I was very, let’s say, valuation driven. I’m coming from that deep value, cigar butt approach. We’ve been looking for cheap companies in terms of low price to book values, low price-earnings ratios, and stuff like that. Good balance sheets, all that stuff.

So, today, I’m saying a company’s valuation is not measurable by a certain number – for example, the price-earnings ratio – but it’s dependent on the quality of the company. The higher the quality of the company, the higher the ratios or the valuations may be justified in a higher range.

Over time, I’ve adapted this approach a little bit. So, today, I’m saying a company’s valuation is not measurable by a certain number – for example, the price-earnings ratio – but it’s dependent on the quality of the company. The higher the quality of the company, the higher the ratios or the valuations may be justified in a higher range. So, this is one example but there are many, many others.

In the soft fact surrounding the way we look at competitive advantages, all these things have changed over time. In the process of learning and getting experience by looking at companies by analyzing companies. So, it just adds up slowly over time and you can’t even say there’s one point in time when we changed this and then that happened. And so, it’s a process and it’s fluid.

The two phases of Alpha Star

[00:06:28] Tilman Versch: That’s interesting. Looking back on your history, you had, I think, two phases. Before funding the fund and after funding the fund. Maybe you can explain the two phases of it.

[00:06:44] Felix Gode: Yeah, sure. Well, the whole thing started when I was in an exchange semester in university. It’s my third semester. I’ve been to the USA, to California. I had a roommate in the place where I was living in. He was also from Germany.

He realized I’m doing all these private transactions. At night in California, it was the time in Germany when the stock market opens so I watch my private portfolio. He said, “Okay. You are so keen on that. You’re so behind on this topic. Isn’t it possible for you to manage some money of mine as well?” So, this was the initial moment where I started thinking about money management. This was the first time.

He said, “Okay. You are so keen on that. You’re so behind on this topic. Isn’t it possible for you to manage some money of mine as well?” So, this was the initial moment where I started thinking about money management. This was the first time.

Over the weeks and months, these ideas emerged. I had no money at that time, or at least not very much. I had no access to investors so there was no chance for me at all to start a mutual fund or any other vehicle. The only option was, and this was quite a good option at that time, we started an investment club.

My brother and I back in Germany started an investment club mainly funded by family and friends. So, really low money in the beginning. This was the time when we started to track, obviously, our track record. This was more like a hobby – what we’ve done. But from the start, from the beginning, we realized quite good returns.

Historical returns

[00:08:43] Tilman Versch: What kind of returns do you have in the history?

[00:08:47] Felix Gode: Just looking at the investment club from 2006 to 2014, there was an average return of about 16p.a. % after fees and after costs. Investment clubs have even higher costs than mutual funds. This was quite good always but we did not do any active selling. We had no marketing, no sales.

But in 2014, we decided to do it more professionally and switched that. We made the investment club into a mutual fund. Since then, we are in a professional framework. And from that point on we developed sales, we developed marketing further. So, we grew over time. Obviously in assets, in management, as well as a professionality regarding sales, all these topics.

What never changed is our focus on what we are investing in. So, German small-mid cap or German-speaking small-mid caps has ever been the topic.

What never changed is our focus on what we are investing in. So, German small-mid cap or German-speaking small-mid caps has ever been the topic. This is definitely a constant in this long process of the new life.

Principles used in building the fund

[00:10:12] Tilman Versch: In your fund, you have this idea of the investment club but you made it somehow better. So, you’re not a classical mutual fund. Do you have different principles on how you’re building your fund? What principles are those?

[00:10:26] Felix Gode: Well, from the structure, this is a classic mutual fund. But our way of thinking, our way of communicating to our clients or to investors, that is a little bit different, I guess, to many other funds.

Our way of thinking, our way of communicating to our clients or to investors, is a little bit different, I guess, to many other funds.

From the beginning on, we set our differentiation. The competition clearly is other mutual funds, also in the very beginning when we still were an investment club. So, we said, “Okay, there must be some differentiation. And this was, in our point of view, transparency. Because transparency, still today, is a major issue. Investors don’t know what happened in the fund, what the fund manager does, and why. This is what we wanted to address.

From the very beginning, we, for example, showed the whole portfolio on our website and we still do. I think we are the only mutual fund in Germany who does it. I don’t know any other. Additionally, we put a lot of effort in communications as a monthly client newsletter or magazine. We share a little bit about the way we think, the way we invest. We share insights to our portfolio companies and all the things.

I think this is an important topic and an important issue. Investors know what’s happening and what the fund management is doing. That gives them a feeling of security, the feeling of being involved. Especially in difficult times, it’s a major advantage. That’s what we experienced also in 2008. For example, in 2020, when the Corona pandemic came over us.

We experience very little outflows of our fund. One point is that our communication strategy keeps people involved and keeps people on board.

Client Structure Changes

[00:12:58] Tilman Versch: So, you build the kind of club that gives you also the kind of capital your investors give in as they are committed to the strategy?

[00:13:08] Felix Gode: Yeah, definitely. This thought of being a club is still alive with us. Over time, of course, the client structure changes, it’s not only retail private investors anymore like in the very beginning of the investment club. Of course, over time professional investors came on board as well. Like asset managers and banks, for example, or family offices. But we all share the same information with every client. And so, everybody who wants to get informed about what we’re doing is able to get this information. I think this is an advantage for every kind of investor. It’s not only preferable for clients or private investors but for everybody.

[00:14:03] Tilman Versch: That’s a good approach and quite interesting approach.

[00:14:09] Felix Gode: I actually don’t understand why not more money managers or fund managers are communicating a bit more openly because it’s known that people are withdrawing money especially when the crisis has come up when people get afraid of what is happening. Constant communication helps clients or investors to be sticky and to understand that this will pass and that better times will come again. Therefore, I’m quite curious about why others are not doing it.

Skin in the game

[00:15:07] Tilman Versch: How much skin in the game do you have in the funds?

[00:15:12] Felix Gode: Personally, I have 100% of my private capital invested in both of our funds. Our team members also have all invested major parts of their private capital in our fund, so we have a lot of skin in the game.

[00:15:31] Tilman Versch: That’s good to hear. And also, friends and family are also fully invested. You have to be careful. Otherwise, your mom will be angry.

[00:15:42] Felix Gode: Well, I would always want the manager I am giving my money to invest in the same strategy as well. I mean this aligns the interests of both parties. I guess that’s the best thing you can have, or you can achieve.

Two Strategies for trading

[00:16:00] Tilman Versch: You have two strategies. What are these strategies? What is the first strategy and what is the second strategy?

[00:16:07] Felix Gode: Well, the strategies are not that different actually. We have two publicly traded or publicly available mutual funds. TheAlpha Star Aktienfonds and the Alpha Star Dividendenfonds.

The Aktienfonds is a basic product or our first product. It succeeded the investment club. This is a fund where we just invest and reinvest the capital gains. The Alpha Star Dividendenfonds is also a mutual fund, which follows the same principles concerning the companies we’re choosing, but it’s distributing cash in quarterly dividends to its shareholders or to its clients.

The Aktienfonds is a basic product or our first product. It succeeded the investment club. This is a fund where we just invest and reinvest the capital gains. The Alpha Star Dividendenfonds is also a mutual fund, which follows the same principles concerning the companies we’re choosing, but it’s distributing cash in quarterly dividends to its shareholders or to its clients. That’s the main difference. One is not distributing. The other one is distributing. It’s doing it quarterly, 1% per quarter, 4% per year. It’s what investors are getting out of these dividend funds.

The universe of companies that Alpha Star has invested in

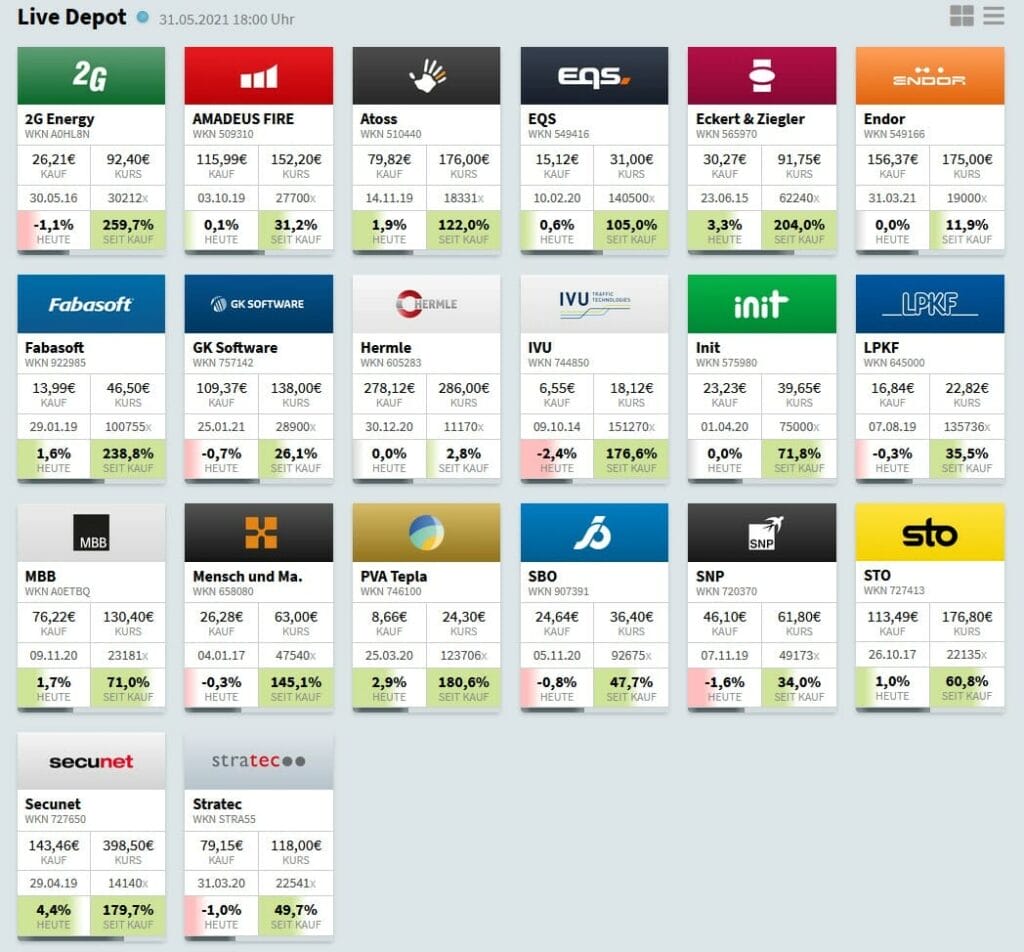

[00:17:29] Tilman Versch: I also want to show the life composition of the Aktienfondsbecause you have it your website. But before we go into details about this fund and look at certain securities, I want to discuss a bit the universe you’re investing in. How would you describe the universe you’re investing in the German-speaking countries like Germany, Austria, and Switzerland?

[00:18:02] Felix Gode: Yeah. Well, it’s not so easy in terms of we are not in terms of industry or something like that. We are not focusing on certain industries, for example. What I love about companies is quality. I mentioned this before.

What I love about companies is quality.

Quality is, of course, a broad range of possible meanings. But what we mean by this is we prefer companies, for example, that grew over time organically. So, what I don’t like is companies that buy other companies over and over again to leverage their balance sheets.

I like proprietary technologies. I like companies that have developed something, product, software, whatever, and have developed those products over time.

That focus on a product and making this better and better over a long period of time. This is what I like the most because if you have such companies those are the companies, which are most likely the ones that have barriers of entry that have competitive advantages because they have put so much effort over a certain amount of years in being the best in that area in which they operate. This is, in a broad sense, what we are looking for.

[00:19:50] Tilman Versch: And how big is the universe you’re covering? I think you once had three hundred stocks or around that number?

[00:19:57] Felix Gode: In the German-speaking country, Germany, Austria, and Switzerland taking the three countries together, we have around 1,500 companies. Our focus is much narrower.

What we are trying to do is to invest in the 30 companies, so this is 2% out of those 1,500 companies. The best 30 companies, this is our type.

What we are trying to do is to invest in the 30 companies, so this is 2% out of those 1,500 companies. The best 30 companies, this is our type. Of course, the watchlist we are focusing on, and we are covering is a little bit broader. It’s like 50 stocks to 100 stocks but the really narrow range, I always compare it a little bit with a football team or something like a little sports team. You have a whole team, but only a certain number of players are on the pitch. Those players in our case are the 30 ones that are in our portfolios. Twenty to 30, 40 others are sitting on the bench waiting to get on the pitch at a certain time. So, the reason why they are out and not on the field is, they are different. This could be because they are too expensive, or the time is not right to get into stock. Several reasons. But what we are trying, 2% of the 1,500 stocks should be on the pitch.

How to avoid companies that play dirty

[00:21:36] Tilman Versch: Germans like soccer but sometimes there are soccer players in Germany that play big fouls. We had a problem with Wirecard and also allegations against Grenke last year. How do you make sure you stay away from such “fraud” situations?

[00:21:57] Felix Gode: Well, you never can be 100% sure, of course. But if you’re focusing on high quality, the probability to get in such a trap is much lower, obviously.

For example, we are focusing on companies, as I’ve described, with a long-standing history and a long-standing history of excellence. Those companies are characterized very often by high returns on invested capital, high cash flows, clean balance sheets. So, if you have a company with a clean balance sheet and not many specialties, not much leverage, not much intangible assets, all these things, and the accounting specialties, like for example, Grenke is a good example. It’s a very complex, very difficult balance sheet, and difficult accounting principles are there. You won’t find such things in our portfolio.

This easiness and cleanliness in the balance sheet and the business model and this whole structure, it’s also a structure of things with companies that reduces the probability of failure a lot, I guess.

Portfolio principles of Felix Gode

[00:23:36] Tilman Versch: Let’s go back to the overview of your portfolio and try to understand a bit how you are constructing this portfolio. So, what are the principles that have led to this portfolio?

[00:23:53] Felix Gode: Basically, we want to have a quite narrow portfolio. It must be, at most, 20 companies. This is what we also see today. There are only 20 companies and there won’t be more. If we add another company, if we say we find another company, then we need to decide which other company should leave. So, this is, I think, important.

The other thing is concerning the single companies that we have a strong focus on return on invested capital. This is our main value driver. We want companies that produce high yields on their capital. These are the main factors, I would say.

We want companies that produce high yields on their capital.

Selling companies

[00:25:00] Tilman Versch: What would lead you to sell a company besides that you found a better one? What are the reasons to sell for you?

[00:25:08] Felix Gode: Well, just the most common reason. Companies change over time. They evolve over time. So, from time to time we find a company which offers a better opportunity. This is a major factor we’re selling.

Of course, there can be reasons concerning pricing. Maybe, say, companies get too expensive. But this is actually not the case very often because as I explained or as I mentioned before if you have high-quality companies with a high return on investment capital and have high cash flows, it’s possible to allow the stock to rise a little bit or a little bit too much. Higher pricing is more acceptable there.

Because you know that this company would grow into this valuation quite soon. Or even more, if that company comes down at some point in time because of high valuation, you always have the opportunity without having to think about buying new shares or additional shares.

So, what do we do if companies are getting too expensive or a little bit too expensive? Then we obviously reduce the weighting in the portfolio, but we almost never sell them because of the high price. We don’t sell the complete position. We drive down to valuation and put the weight on cheapest stocks a little bit higher so the impact if the valuation is coming down, is not that big on the portfolio. But if you have a great company, there’s not really a reason to sell it completely.

The 5/10/40 rule in portfolio construction

[00:27:23] Tilman Versch: With 20 stocks, you have like 5% position for every position. In the medium, how big can your positions go – from just 1% till 10%? How are you sizing?

[00:27:40] Felix Gode: As we are a mutual fund, we are bound to certain rules. So, you might be familiar with the 5/10/40 rule which says not one single stock is allowed to be bigger than 5% in weighting. But there are exceptions, and the exception says that a certain amount of stocks can be up to 10% in weight, but all these exceptions together cannot be more than 40%.

So, if you take this 5/10/40 rule, and you also take the need to have a quite narrow portfolio, then the consequence is you can do an overweight on four or five stocks and all the other stocks are in a very regular weighting of 4%. So, in a portfolio of 20 stocks, we have 15 stocks at 4% and we have five stocks at 7%. So, this is roughly the size we are aiming at.

What’s special about Endor, Felix Gode?

[00:29:08] Tilman Versch: That’s interesting. Maybe let’s go into detail about some of the stocks you have in your portfolio. You have one stock that’s also quite common for some of the American investors because it was one of the stocks that were also kind of promoted internationally. It’s Endor. What is Endor doing and why do you like it?

[00:29:32] Felix Gode: Yeah. Endor is a wonderful example of the high-quality companies I mentioned before. I mean, they’re doing gaming equipment. It’s a really easy-to-understand business model. They are doing the steering wheels, wheelbases, and gear shifts, and so on. The paddles for SIM racing, so for computer games, for computer gamers. But they’re focusing on the high-end segment of that.

The products they are producing are comparable to what you buy in a toy store somewhere for your kids, but they are high-end, and they are simulating real-life experiences. They are used as well in real life. For example, they’ve made a steering wheel for a BMW. You can use it for gaming, but it’s actually used in the BMW GT3 racing car. It’s the same.

This company focuses only on this narrow range of products and has put all its focus over many years on getting better and better in improving quality and experience with these products. So really a niche market they are thrusting but they’re the leading ones. They have a market share of like 80% or something in that area. That’s really, really interesting.

They are the leading company you see by all the partnerships they have. Obviously, partnering with the game console producers like Microsoft, Sony for X-Box, and PS PlayStation. But also, they have corporations with racing associations like Formula 1 and NASCAR and World Rally Association or Championship. But also with the car manufacturers, they are partnering with BMW, Porsche, and so on.

So, you see they are really on top of the whole gaming or a whole SIM racing industry. And this is what makes it interesting. And that’s what you see in the numbers as well. So, if you look at the growth history over the last couple of years, they have been growing tremendously and that’s with quite high margins and additionally, they have slow asset business, you know, so they have put their brainpower into the product over the last couple of years and this materializes over time. This is one perfect example. Those are companies we love.

Discover the Plus Investing community 👋🏻

Hey there!

Discover my Plus community! The community is great for passionate, professional investors.

Here, you can meet investors, share ideas, and join in-person events. We also support you in starting and scaling your fund.

Founder-led companies

[00:32:40] Tilman Versch: the company is founder-led, I think? What percentage does the founder own? Do you know the number of your head?

[00:32:45] Felix Gode: I don’t know off my head. 40% to 50%, something like that. 40%, 30%.

[00:32:51] Tilman Versch: Is this important for your approach to have founder-led companies or?

[00:32:57] Felix Gode: Not necessarily. I like that. This is like we had before. If the founder is involved in his own company, he has skin in the game, you have the same alignment of interest like when I am invested in my own fund. So, this is definitely something we like, but it’s not a must-have.

Not necessarily. I like that. This is like we had before. If the founder is involved in his own company, he has skin in the game, you have the same alignment of interest like when I am invested in my own fund. So, this is definitely something we like, but it’s not a must-have.

What’s special about IVU?

[00:33:25] Tilman Versch: Another company in your portfolio that is, I think it’s quite long in there, I see it’s from- you bought it 2014, is IVU. What do you like about this company?

[00:33:37] Felix Gode: Well, the same thing here. They’re addressing a niche market. This market is big enough to give this company an opportunity to grow over a long period of time. And that’s what they have done.

They’re addressing the public transport market and the rail market with software solutions. So, ERP systems, organizing systems for those public transport companies. All this digitalization that is happening around us is of course given them tablets.

And also, here you see it in the numbers. If you look at the growth rates over the last couple of years and the development of the margins. So, the scaling of the business sets in over the years. Actually, we have this company even longer. I guess we had it since 2007 or 2008. I can’t even remember. Maybe 2009. So, the first price we bought IVU was 1 €.

[00:34:56] Tilman Versch: It’s at 18 at the moment.

[00:34:57] Felix Gode: This is a real long-term. I guess it’s the longest engagement in any stock we have.

Playing the long-term game

[00:35:04] Tilman Versch: That’s quite interesting that you’re really a long-term shareholder and are willing to be invested in the company for the long term.

[00:35:13] Felix Gode: Yeah, this is what we aim for. It’s not always working because, of course, things change. Things might happen. As we have a very narrow portfolio, it happens that there’s a change in the portfolio. But I guess over the next couple of years, it’s probably, less turnover necessary than it was before in the last couple of years. Well, at least for the moment being, I can say I feel quite comfortable with the portfolio we have, the companies as a whole.

If you just look at 2020, those companies we own right now have developed very well despite the recession, despite Corona, because they are focusing on growing or they are active in growing markets. I really feel comfortable right now with the portfolio. I think there will be less turnover actually than in the past.

If you just look at 2020, those companies we own right now have developed very well despite the recession, despite Corona, because they are focusing on growing or they are active in growing markets. I really feel comfortable right now with the portfolio. I think there will be less turnover actually than in the past.

Best way to find stocks

[00:36:24] Tilman Versch: Are you a pure bottom-up stock picker in your approach? Are you investing around certain topics as well?

[00:36:34] Felix Gode: It’s pure bottom-up if you want. I mean, I’m doing this for 18 years and it’s a limited number of companies you have in the German-speaking market. So, I would say I know most of them, at least roughly.

Additionally, in my opinion, it’s the best way to invest. So, go take one stock, look at it, decide what you do, kick it out, or go further. Then, take the next, and the next, and the next. I think that’s the best way to find the best stocks.

Of course, from time to time you read something, you get an idea about a certain industry, a certain trend. And then, I think about, “Okay. What companies do I know which could benefit from this certain trend?”

Then, of course, I am not buying this company blindly. Of course, I do the whole process of analyzing the stock and checking if that hypothesis might be true that this company is profiting or benefiting from this certain trend.

I can say one example. We’ve been thinking about the whole electric car and battery business lately. We have been thinking about what company might be interesting for us in this environment. But you have, of course, in the small-cap sector and in Germany, no possibility or not too many possibilities to invest directly. I mean, VW or BMW would have been a nice investment, but it’s totally out of our scope. We don’t invest in such large companies.

We are always thinking one step further or two steps further. And, have a look at the companies that might indirectly benefit from such trends. So, this is what you obviously have to do many times in the small-cap segment because there are just no direct players. I could not invest in Tesla-like stock in the small-cap EV market. But you must see who is delivering certain parts, certain batteries. Or in this special case, the batteries. That’s the way we approach if we do this kind of industry.

Apply to Good Investing Plus

[00:39:37] Tilman Versch: One new addition of yours called GK Software. What do you like about this company?

Where will Alpha Star be in 5 years, Felix Gode?

[00:39:37] Tilman Versch: That’s an interesting method and a good method, I think. Looking out in the next five years, where do you see Alpha Star then?

[00:40:34] Felix Gode: Yeah. Interesting question. What we have done so far, and we’ve talked about it in the last couple of minutes, we are focused on the German-speaking market so far. But of course, this market is limited. We intentionally keep them quite small.

For example, the Aktienfonds. We closed it at a volume of 50 million just to give it the opportunity to grow return over the next couple of years without having to leave our focus, without having to change our strategy. This is the intention because the outcome will be that we have the potential to achieve those returns that we’ve achieved in the past also for the next couple of years. So, this is the most important point or most important topic for us.

We are intending to set up a new fund which is covering the Alpha Star strategy on the European market. For that, we are setting up the sales right now. We are expanding in the area of sales and marketing

But as I said, we try to invest in 2% of the best companies in the German-speaking market, so obviously, the volume is limited. So, for the next five years, you will see a new mutual fund we are setting up but with a broader range in Germany. We are intending to set up a new fund which is covering the Alpha Star strategy on the European market. For that, we are setting up the sales right now. We are expanding in the area of sales and marketing. And of course, we are looking for new people, fund managers, portfolio managers, who bring know-how about the European stock market, about a European small-mid cap landscape into our company because we cannot cover this on our own, of course.

[00:42:43] Tilman Versch: Do they have to work in Augsburg?

[00:42:46] Felix Gode: Well, that’s a difficult topic. Preferably from my point of view today, it’s an advantage because investing is a lot about talking to each other and exchanging thoughts. And this, of course, is possible nowadays via video conferencing or traditional calls, but it’s not the same.

So, if you take your time, if you talk about, I don’t know certain topics about, is a certain thing about a company a competitive advantage, yes, or no? So, if you have a desk discussion, it’s much more effective, I guess. If you take your time if you talk about that and think about it quietly. I have the feeling that video conferencing is not that relaxed as if you’re sitting on the couch with a coffee in your hand and jointly thinking about things.

But of course, I would not totally exclude this as an option. I mean, the possibilities to communicate clearly are there. This is certainly not a no-go, but I guess there are slight advantages on being present.

[00:44:25] Tilman Versch: So, if there are any investors interested to apply, I will add a link below so people can find the job offers if they are still open.

[00:44:37] Felix Gode: Yeah. That’s a good idea. I’m really looking forward to anybody who is interested in working with us. And, I mean, it’s a nice project. What we have achieved with Der Alpha Star Aktienfonds is that we are leading the rankings in Germany over a couple of years now. That’s what we want to achieve in Europe with the new European fund as well. I mean, it’s a project that is built up from scratch so there’s nothing there yet. But of course, we have the selling power and we have the marketing power which we can use as soon as we start. I think it’s challenging and a very nice opportunity for anybody who’s interested in the European stock market.

Follow us

Management evaluation

[00:45:40] Tilman Versch: That’s good. I’m happy to share this. For the end of our interview, is there something you want to share that we haven’t discussed that might be interesting for the viewers?

[00:45:51] Felix Gode: Maybe one aspect that is important for us which we have not been talking about so far is the whole topic about management evaluation. So, what you often hear if people or investors are assessing management quality and talking about personal things. Of course, their management must be trustable, must be reliable, all this stuff. Of course, it’s important but the thing is that we think that we can measure the quality of the management as well.

We think that we can measure the quality of the management as well.

For example, what the management team can do is control the balance sheet. And so, if you have a look at the balance sheet, you’ll see how the management is operating, how the management is doing their business. So, are they capitalizing on intangible assets, for example? Are they leveraging? Are they growing inorganically? Are they doing many acquisitions, all that stuff? So, the quality of accounting principles or the way they address accounting principles, the way they want to shape their balance sheet. All this is an indication of how the management is thinking and behaving. This is maybe one thing.

And the other point is of course the whole capital allocation topic. I mean, I said it before. Our main driver or the main value driver is the return on invested capital. And of course, this is then the main driver for growth as well. So, if a company has a high return on invested capital, then the capital allocation decision is crucial for growth. Growth is a function of the quality of the business in terms of return on capital and reinvestment. It makes a difference if the management decides, for example, to make an acquisition with a certain amount of available money, or if they are, for example, reinvesting the capital into their own business in terms of development of new products or the exploration of new markets and stuff like that. So, this is of course a critical point because it’s all coming back to the topic of return on invested capital and growth as an important value driver in the long run.

Outro

[00:48:29] Tilman Versch: Very interesting point for the end. Thank you very much for taking the time. Thank you very much to the audience as well for listening to this interview.

[00:48:37] Felix Gode: Thank you for having me. It was fun talking to you. As I said in the very beginning, my first interview in English. I hope I was understandable, or it was understandable.

[00:48:47] Tilman Versch: I think you are.

[00:48:49] Felix Gode: Yeah. If there are any comments, or if you would want to know anything else, of course, you can contact me anytime. Of course, we can talk in German then as well, so it is better to understand

[00:49:03] Tilman Versch: Thank you very much and thank you for the invite.

[00:49:06] Felix Gode: Thank you.

[00:49:08] Tilman Versch: Bye bye.

[00:49:09] Felix Gode: Bye bye.

Disclaimer

Finally, here is the disclaimer. Please check it out as this content is no advice and no recommendation!