How does Creditas contribute to VEF’s success, Dave Nangle?

VEF is the Emerging Markets Fintech investor. The Sweden-listed company is investing in Fintech assets in Emerging Markets. After one year I did a follow-up discussion with CEO Dave Nangle. Here you can find our last conversation.

We have discussed the following topics:

- Check out Interactive Brokers

- Introducing Dave Nangle

- Competitiveness in emerging markets

- Observation of emerging trends

- Toolbox to reach the 30% and not overpay

- The play between numbers-crunching vs. qualitative factors

- Thoughts on optionalities

- VEF’s services

- Borders of founder’s focused ness

- VEF’s strengths

- Increased competition?

- Reasons for deal failures

- Coping with powerlessness and frustrations

- What will happen with NAV?

- Dave Nangle, are down rounds ahead?

- Macro impacts on company valuations

- Brazil

- Dave Nangle on capital allocation

- Listings

- Cash

- Insight into two portfolio holdings: Creditas and Konfio

- Community exclusive: Expectations for the cooperation between Creditas and Nubank

- Creditas’ loss

- Creditas’ efficiency in customer acquisition

- Recurring and upfront revenue

- Dave Nangle on rethinking sizing

- Learnings from the Russian conflict

- Konfio’s future

- Interesting learnings

- Dave Nangle on the next Creditas?

- The next Konfio?

- Egypt

- Playbook to open new markets

- Climate risks

- Dave Nangle's closing thoughts

- Thank you

- Disclaimer

[00:00:00] Tilman Versch: Find the link to this episode here, the VEF Share price, NAV/share and the premium discount chart at [00:20:35] and the Creditas’ chart at [00:47:46].

Check out Interactive Brokers

This episode of Good Investing Talks is supported by Interactive Brokers. If you’re ever looking for a broker, Interactive Brokers is the place to go. I personally use their service because I think they have a great selection of stocks and markets you can access; they have super fair prices and a great tracking system to track your performance. If you want to try out the offer of Interactive Brokers and support my channel, please click on the link below. There, you will be directed to Interactive Brokers and can get an idea of what they offer for you. I really like their tool and it’s a high recommendation by me. And now, enjoy the video.

Introducing Dave Nangle

[00:00:38] Tilman Versch: Hello audience. It’s great to have you back and I’m also very happy to welcome Dave Nangle of VEF VC. www.vef.vc is their website, but they are not a typical VC and we already discussed this in the last interview you can find above here. It’s great to have you back, Dave.

[00:00:58] Dave Nangle: Hey, thanks, Tilman. Great to be back.

Competitiveness in emerging markets

[00:01:00] Tilman Versch: It is very nice to do our interview after one year because a lot of dynamics in the markets have changed and we really have a different situation at the moment.

We already talked about this in our pre-talk and at the beginning of our interview, I want to try to figure out a bit the dynamics between public and private markets. So, Dave, in your position at VEF, you have a lot of insights into private markets as a long-term oriented VC investor in different emerging markets within the FinTech space. So, what could you observe in just markets? What are especially hot markets with a lot of competition and which markets don’t have that much competition?

[00:01:46] Dave Nangle: More and less competitiveness in the private markets within FinTech across emerging markets. Look, I wouldn’t say it’s a natural kind of consistency across the board. Generally, I’ve seen emerging markets a lot more by country than by segment over time. So, we kind of get countries being hot as opposed to segments themselves being hot. India, I think, has always been at its prime because China obviously is fascinating, big, and a massive opportunity, but then generally, China is for the Chinese. It is the way most investors see it.

So, India, as a country, has always been a hot and true cycle. And behind that, not too far behind, I say it’s Brazil. And then everything else kind of flows in and out of kind of temperature – hot being Mexico, being Southeast Asia, Africa – front and center gets a lot of focus more so than other countries on a similar pecking, I would say. Maybe like the Pakistans of this world or parts of Southeast Asia, Africa always has a lot of dedicated capital, whether it’s the ESG side of financial inclusion money, or just, generally speaking, it’s very much a focus continent for capital. But I’d say that’s the true cycle. India, Brazil – I would put them top two and very much in focus.

India, as a country, has always been a hot and true cycle. And behind that, not too far behind, I say it’s Brazil.

If it was going to drill down to sectors, like payments always gets to focus and it was online, offline, definitely cross borderless so, and then credit kind of comes in and out. But I guess more and more, we’re seeing a lot of Web 3 focus and it’s the future of financing Web 3 in various forms of blockchain technology and cryptocurrencies. We’ve seen the volume turn up there from very focused investors to a more mainstream investor base focusing on that space.

Observation of emerging trends

[00:03:39] Tilman Versch: So, if you look at hotness, it also attracts more competition, and this leads to the risk of overpaying if there’s more competition in a certain space because there’s only a limited number of great companies. And if a lot of demand for them is around, prices go up. So, with your focus in emerging markets and FinTech, do you see this happening in a lot of markets or what do you observe there?

[00:04:12] Dave Nangle: Look, we’re talking today, and we probably would have had a different conversation three months ago than today. I love emerging markets. I’ve been doing emerging markets all my career and part of that love affair with them is partly due to a lack of competition. You just get fewer eyeballs, less capital, and less skill set focusing on the biggest part of the world, the fastest-growing parts of the world, and the most fascinating part of the world. Never linear in nature, but generally going up into the right gradually over time. And then, you get periods over the last five to 10 years where we had a good run.

I’ve been doing emerging markets all my career and part of that love affair with them is partially due to a lack of competition.

We had a good run for global stability, global macro capital flows into the private side, venture funds, and private equity. And we started this seven years ago and we would’ve been alone and shopping in Pakistan, for example. You fast-track it today, it’s busy. And if Pakistan gets busy, you start to ask questions, you know, what’s happening in the world, no offense to Pakistan.

Brazil, back in 2016 at the back end of the last kind of mini-recession, we were not alone but we were one of the few kinds of series VC investors who were turning up in that market, picking up names like Creditas, same in Mexico, picking up names like Canfield and you fast track to 2021 and it got very busy. But then, your kind of fast track a little bit to today, and what you’re seeing is the start of a risk-off mode globally, you know, privates taking their lead off Publix at last. It took some time when they got there.

So, I guess what I’d say is we are a permanent capital vehicle, we’re true cycle investors, we’re long-term investors and these aren’t cliches, these are facts. We haven’t just raised the funds that we have to deploy capital in order to get paid. We could not invest for a period. We can stop and watch markets for a year, for two years. We cannot invest in Mexico for five years and then do five investments in Mexico. And should we see fit if the time is right if it’s a window where political instability currency blows out and the opportunity set arises?

So, I love that flexibility and over time, we’ve kind of got a checklist of what we’re looking for in a company. And we’re very rigid and disciplined in that and we don’t get everything we want. We just don’t invest. Not saying we can’t invest, but we want great founders, we want great VCs around that founder, we want traction, strong unit economics, a big addressable term, good regulatory support, and defendable moats. If we get all that, we dig in and we go deep. But then, we’re looking for valuation also, and 30% IOR is our hurdle rate.

Over time, we’ve kind of got a checklist of what we’re looking for in a company. And we’re very rigid and disciplined in that and we don’t get everything we want. We just don’t invest.

Now, in fairness, as you alluded to over the last 12 to 18 months, we started to ask ourselves, “Are we wrong?” because we were losing deals and we were losing more deals than we did. And we were losing them mainly on valuation where other people were willing to pay more. So, we’re trying to ask ourselves, are we in the wrong game? Is 20% the new 30%? But then, you fast-track it today and the question is, is 40% the new 30% in a higher-risk environment? Is 30% enough to put your dollar to work in an emerging market?

So, these cycles come and go. Some are longer in duration than others, but I’m very comfortable that we have a playbook of what we want to find in an investment, and what we look for. And we find out trying to get our capital in at the right valuation and even in periods which are hot and cold, we generally converted on a regular basis and found what we want. So, even last year when deals were passing us by for evaluation, we still got our capital into names like Rupeek and the gold back lending space in India, into Black Book. And we’re then putting more capital to work in some of our better companies like Credit Us and Konfio. At each time, we were justifying it with 30% IORs and excel on paper with the money we were putting into work.

So, busier – yes. I expect that volume to turn down and I kind of expect global capital, which ventured outside of the US, Europe got a bit more aggressive during the pandemic specifically via Zoom in markets where it’s not their first protocol – that’s no offense to them – but getting capital to work out of the US into Nigeria or into Pakistan or investing in Brazil having never traveled there, and that’s not sweeping a statement as isolated incidents. I think that capital starts to go a little bit more risk-off and for people like us, true cycle investors, it’s going to be a very interesting next six to 12 months. And these are the kind of windows where we can make some very interesting bets with a five-to-10-year view on the horizon, you know, on the lookout.

Toolbox to reach the 30% and not overpay

[00:08:36] Tilman Versch: So, let us take a look at your toolbox. So, how do you arrive at this 30%? How do you measure them and what is in your toolbox for the 4% return?

[00:08:47] Dave Nangle: The toolbox. Well, it’s analysis, it’s getting into the companies, it’s forecasting. So, every company we look at, and we’re generally looking at series B, C, that kind of area, and they’ll have their own numbers and forecasts from an individual company point of view. But we’ll be stress-testing the hell out of that and their numbers out three to five years. If it’s a realistic model we’ll work with it, if it’s unrealistic, we’ll build our own. But we’re generally trimming and being more conservative than what they’re being.

The toolbox…well, it’s analysis, it’s getting into the companies, it’s forecasting.

And they should be aspirational – they’re entrepreneurs, it’s the game that they’re in. And forecasting out in local currency because these are all local currency businesses that we’re investing in for the most parts, be that Mexican Peso, Turkish Lira, Brazilian Real and deflating that when we convert hard currency into US Dollar because the assumption is the currency will weaken over time. So, maybe, a currency deflator is five to 10% per annum, depending on the market.

And then we’re looking at exit multiples as you look five years out. We’re looking at the peer group, we’re looking at a reasonable peer group and an exit average multiple over time for these companies and that’s the exit month we’re putting on these companies. And then we’re discounting it back to see if we can get, for the price we’re paying today, what would be the price we’d pay today to get a realistic 30% plus IOR on our money.

The play between numbers-crunching vs. qualitative factors

[00:10:04] Tilman Versch: So, are there any qualitative factors in your 30% calculations or is there any founder’s premium because the founder is so good, or is it just numbers-crunching?

[00:10:17] Dave Nangle: It’s numbered crunching, and we don’t crunch the numbers if the founder isn’t right. So, the qualitative factors are what get us to spend the time on the numbers and we’re not going to waste our time on numbers if those qualitative factors don’t work.

So, the founders, the VC, the space, the scalability, the addressable market, all that kind of stuff makes us want to do work because time is an asset, Tilman. We are a small team, well, small and growing; we’re nearly 10 people now. So, we’re growing as a team, as our AUM grows, as our business grows. But still, the opportunity cost of us spending any time on one individual company that we’re not going to invest in is hard. So, we sit down once, twice a week as a team and decide where we’re going to spend our time, interacting with our IC, which is our board, about where we should be spending time, what they would or would not approve if we do spend our time.

The qualitative factors are what gets us to spend the time on the numbers and we’re not going to waste our time on numbers if those qualitative factors don’t work.

So, all those qualitative factors feed in, and then obviously, we’re getting into the number side of things, which is our strength, it’s our history. I guess we came into this, not as founders, but as analysts, as research people, as investment managers. A lot of people enter the VC world or private equity world as former founders. And everybody has a strength, brings something different. I think we’ve learned those skills and those muscles, but we brought discipline to numbers.

And I guess that’s where we feel comfortable today with markets obviously dislocating and share prices falling. Did we get caught in the up cycle where we’re playing top-of-cycle multiples for investments, we did just 3, 6, or 12 months ago? I don’t think so. I think we’re very respectful of shareholder capital. We turned down deals that were wrong. We were playing true cycle multiples albeit now we’re at the lower end of cycle multiples. So, I think that’s the discipline which served us well or will serve us well, let’s say that.

Thoughts on optionalities

[00:12:00] Tilman Versch: So, in your calculations, what value do you address to options with creditors? You had them going to different verticals and enhancing their business. Is this something you factor in, for instance?

[00:12:14] Dave Nangle: Now…it’s fair. We forecast what we can see, Tilman. New countries, new business lines, we’ll do this and that and we’ve seen it again and again, where companies say, “We’re going to go here, there, we’re going to roll out this and that’s worth something.” It might be worth something to them…it’s not worth anything to us. It’s nice to see. It gives you comfort that they’re ambitious, but we forecast what we can see. We underwrite what we can see and then, we’ll take whatever else on top when it comes.

VEF’s services

[00:12:41] Tilman Versch: So, coming back to this idea of competition, and you already mentioned that you don’t want to overpay and have a clear limit here, but is there also some impact of competition on your service side so that you said VEF had to increase the offering it gives to founders, get more founder focused, get better in this, and is there any strength you want to add over the next years for VEF in this matter?

[00:13:12] Dave Nangle: Yeah, no. It’s an interesting question and we do think about this a lot as one of our goals is to be the number one investor for the companies that we invest in. We obviously need to take care of our capital, which is our shareholders and take care of our companies, but if we are a top-ranked investor in their NPS or their scoring internally, we will have a good brand and reputation in that market, be that Brazil, be that Mexico, be that India. And that will roll onto us getting invited to other great assets potentially to invest in.

So, I think first and foremost, you need to be supportive as a shareholder. We’ve learned that. And over time, you need to work with these companies in good times and bad. You need to provide capital and be a good supportive shareholder and tell them what you think at the same time.

You need to provide capital and be a good supportive shareholder and tell them what you think at the same time.

I think that’s key. I think from our side where our strength is, as I said, in numbers and forecasting and modeling, especially early-stage companies, we stress test the hell out of their budgets and their models. We help them prepare for fundraising, we’re very strong in capital raising be that debt or equity. So, we’re kind of like an internal consultant or an internal investment bank for these companies.

We don’t overplay our hands. There are other funds that we partner with which are very strong in different areas; the likes of QED, the Capital One guys, these are very strong in data and asset quality, and the guys at Kazakh in Latin America – they’re ex Mercado Libre guys. They’re great in scaling unit economics. They have real strengths in having built businesses from the ground up in that continent. And if everybody brings their core skillset to the table, in general, wisdom set, then it benefits the company and the founders in their journey. So, we play to our strengths.

What have we got inside a team? It is a team of basically fundamental analysts and investors, and we could add founders to that, some skill set around that, and we haven’t gone there yet, but it’s possible.

What have we got inside a team? It is a team of fundamental analysts and investors, and we could add founders to that, some skill set around that, and we haven’t gone there yet, but it’s possible.

Borders of founder’s focused ness

[00:14:59] Tilman Versch: What are the borders in your founder focussed ness? So, what are examples where you said you get some in crisis, but you finally said, “we can’t help you”?

[00:15:10] Dave Nangle: So, a founder comes to us and asks for help in a specific area, and we go, “no”, is that the question?

[00:15:17] Tilman Verch: Say, “This is something we can’t do. We would love to help you, but we don’t have the capability to help you.” So, what are the limits here?

[00:15:33] Dave Nangle: Exactly. Look, I guess there’s an element of we shouldn’t be telling companies how to run their business. We’re the investors, we’re investing in people who should have an idea of how to run their business, and where we’re going. We should be the sounding board, a strategy. We should be the stress test and not looking to trip them up.

There’s an element of we shouldn’t be telling companies how to run their business.

And we’ve got investors like that where I was in the US last week, and we sat in a room with investors for an hour, for two hours. People like Fidelity, people like Ruane Cuniff and they were stress testing us, being slightly pushy, but it was for our benefit of us. So, we’d walk away from that meeting and think and think twice about our strategy, what we’re doing, and aspects of it so that they would benefit as shareholders. So, I love doing that. Then with my company, it’s just softly pushing them around a bit so that they rethink everything that they’re going to do next, which I think they may have dug into.

But, in areas like skill sets, we will definitely liaise with outside experts in tech, in credit quality and connect people outside of our own company, but skill sets and people that we know in our portfolio companies, we don’t have that skill set. We’ll never just give a hard no and go, “no, we can’t help there”. It’s always got to be some caveat of, “let’s see how we can help”.

We’ll never just give a hard no and go, “no, we can’t help there”. It’s always got to be some caveat of, “let’s see how we can help”.

VEF’s strengths

[00:16:43] Tilman Verch: And where do you see your strengths in helping companies? You already mentioned that a bit in reference to founding rounds and helping companies to access more money.

[00:16:54] Dave Nangle: Yeah. We do a lot of work in that area. I think it’s important. I think capital raising is key. It’s key to the success of a private company. You can have a great company, a strategy, and numbers, and if the founder or founding team hasn’t got the skills to raise capital, and there are some soft and hard skills embedded in that, it can be trained.

So, we work very closely with these companies to get their pitch right and their presentation right to be presenting the right story in the right way. And that’s a key area I think we focus on, and in introductions to anybody in our ecosystem and they’re warm introductions because we wouldn’t be introducing a company if we didn’t rate it ourselves and put our own capital to work in it. So, I think that’s kind of a forte for what we do.

We work very closely with these companies to get their pitch right and their presentation right to be presenting the right story in the right way.

Increased competition?

[00:17:37] Tilman Versch: So, again, back to the idea of competition and…what had the increased competition and increased demand for great companies has led to higher shares of passes for you either because the company said “we don’t want you” or the valuation was too high for you? How did the share of passings develop over the last time?

[00:18:03] Dave Nangle: It’s definitely grown. It was definitely probably our peak year in 2021 on that front, but maybe it’s worth pulling back to the fact that we probably convert 1% of the deals that hit our funnel. So, last year we looked at over 300 deals as a team and that’s from a first call right through to full due diligence. And sometimes, things hit our process and it’s a 30-minute call and that’s it, it’s logged in the system, and we move on. But to answer your question, last year, we did three deals, I believe, and we lost three deals because of valuation. As in, we wanted to invest, we were ready to hand the term sheet or did hand the term sheet and somebody else turned up with an evaluation higher in one instance, twice as high.

And in that instance, all you do is you call the founder and say, “congratulations”, you know, “good for you, you’ve got a bigger check from arguably a bigger fund than a bigger valuation, less dilution. We were here to invest on reasonable terms, but congratulations and there’s no disrespect and it’s all good”. So, I’d say 50% of the time last year. And before that, very seldom it happens to us in 2017 through 2020, but 2021 was definitely busy on that front in terms of getting refused, Tilman. Yes, at the door.

Reasons for deal failures

[00:19:20] Tilman Versch: What are the other reasons a deal in the end-stage besides valuations, didn’t go through?

[00:19:27] Dave Nangle: Yeah. Like, if we get to that stage, it’s because we’ve done everything on our site from due diligence and numbers and point of view that we want to do it. Legals are obviously a key area that can stop a deal from happening and to be quite honest, our chief council can veto any deal that we’re doing based on legal in terms of terms and because, obviously, last year and the last 18 months, as well as valuations and competition going up because the hotter companies and the terms start to get looser for the investors. So, you’re getting a smaller stake for a bigger check. You’re getting fewer legal rights. All these things turn to loosen up by the top end of the cycle. We haven’t had it yet, but our chief council can very much step in and say, “we’re not doing this deal because the rights that we’re getting here are not comfortable for us as a company and for our shareholders and the capital that we represent”. So, it doesn’t get their easiest valuation, but legal can be another thing that just stops it at the last stage.

Our chief counsel can very much step in and say, “we’re not doing this deal because the rights that we’re getting here are not comfortable for us as a company and for our shareholders and the capital that we represent.”

Coping with powerlessness and frustrations

[00:20:26] Tilman Versch: You know this chart very well?

[00:20:29] Dave Nangle: I’m about to find out…

[00:20:30] Tilman Versch: It’s loading. It’s the NAV price chart and it’s not the latest numbers we have here because like your share price is a bit down more and the discount NAV has even widened from here.

So, with this chart in mind, let me ask a personal question. What does this, do to you, on a personal level, you do a lot of hard work, a lot of travel, and so forth, but things run against you for a while and this market. And as an investor myself, I know it feels a bit powerless in these periods of time. You do your work, you reposition yourself, but it’s like the results don’t look that good. How are you coping with this powerlessness and may be frustration, or anger that comes up on a personal level? What are your hacks to stay focused and stay aggressive and don’t lose the love for the game?

[00:21:27] Dave Nangle: It’s a fair question. Actually, I’m very unemotional about share prices. It’s a chart, it’s a number, it’s a data point. If you get into the day-watching of share prices on your own share price, you will go mad. I think I learned long ago that the macro overrides the micro every time. So, if Russia invades Ukraine if growth stocks are out of favor, and if the US, if the S&P or NASDAQ is falling, who am I, or VEF share price, to get in the way of that? It’s going to happen.

If you get into the day-watching of share prices on your own share price, you will go mad.

I look at our history over seven years and what we’ve achieved and what we’ve created and the position that we’re in today. I look forward and I get more excited about dislocations and opportunities to compound value from here and once we defend and get everything on the front foot as is key. I fully understand we’re all learning but, markets are, for us, they’re a higher beta representation of our NAV per share. So, our NAV per share may go gradually and generally up to the right, but we see the share price, you know, bounce around aggressively as it does – markets are efficient, sometimes overly so – they overshoot on the way up. As we go to a premium, they overshoot on the way down. As you go to a deep discount…yeah.

I respect markets, I watch markets, they obviously impact us as a company, our valuation, when we can raise capital, what do we buy back, et cetera. Opportunities arise from that. But no, I don’t get disheartened. I get out there like I did last week, and I meet investors, I hold their hand, and I tell them what’s going on. I meet new investors and I warm them up for the next time and we just keep on working. We communicate, we do things like this. We get out in front of investors, we don’t hide. And over time, that will all take care of itself.

We get out in front of investors, we don’t hide. And over time, that will all take care of itself.

What will happen with NAV?

[00:23:35] Tilman Versch: A lot of the next questions are a bit in the core, the concern of some investors who are public investors that there’s a disconnection that “I’m coming from the private markets” and the valuations we see in the public markets and the end, private market valuations will go down to the public market valuations. And, for you, it is an important exit way to get money in the public market again.

So, what do you think is more true: if the current discount to NAV Mr. Market is telling you that the IP of creditors, I think it’s scheduled for 2023 but correct me if I’m wrong here, will end in a down round if they go public, or Mr. Market is currently depressed and valuation should recover in the next three years to the levels you are shown with your NAV? What do you think is truer, or is there anything in between?

[00:24:29] Dave Nangle: So, dislocations between public and private markets are vice versa. Well, what are we? We are a listed entity, so we have a share price. Who are our shareholders? Fidelity, Wellington, Rubico, Fidelity. As private market investors, we are as connected to the public markets as can be. So, we’re not a Sequoia or Excel or big venture capital or private equity house, and that’s no offense to them either, but we are very connected to public markets, and my history, and most of the team’s history, is in public markets. So, we’ve got a great understanding, and respect and we’re always learning about public markets. So, we don’t live in a private market bubble where we believe that private companies should trade at 10 times what their public period should trade at. We know there’s a connector, and we know when you’re exiting, if you are exiting via IPO, private markets meet public markets, and reality kicks in eventually. So, you always need to keep that in hand, and that’s how we value companies on an ongoing basis.

As private market investors, we are as connected to the public markets as can be.

So, that’s just one aspect of saying that from a general point of view. Then there’s our NAV, and our NAV is made up of our portfolio companies and the valuation that we hold those companies at. And we’ve got to respect the fact that share prices have fallen in global markets, and then within that, there are certain country share prices and certain sectors that are key peers for the companies that we invest in.

But what I’ve been talking to investors about is, that it’s one aspect of an evaluation in a company like ours. We have underlying forecasts and performance of our companies, growth of those numbers. We have local currencies translating that back into dollars. So, we take something like Creditas, and that’s key to talk about because it is our biggest asset. They did raise money in Q4 of last year, and we did put capital to work in that. And one of our big investors, Fidelity, led that round. And they are public into private, they’ve got their finger on the pulse. Wellington, who is also an investor in us, took part in that round. They’re public. So, there are lots of public-private crossover people knocking around the credit task table. So, it’s not ignorance of private markets.

And then, you look at some of the periods and the share price fall-off year to date versus, say, Creditas. And maybe they fall in 20%, maybe some will fall 40 to 50%. But then, I look at Creditas as numbers and they’ve grown 20% plus quarter and quarter in Q1. So, the underlying growth in the story is supernatural versus periods. Then I look at the Brazilian Real versus US Dollar, and that’s nearly strengthened 20% quarter and quarter in Q1.

So, you’ve got these conflicting factors as opposed to, you know, I see a share price of PayPal or Sequoia where it’s fallen 30% i.e., your Creditas position is worth less. So, I guess that’s what we talk to investors about, and we’re very specific on each company that we look at. There are individual forecasts and performance to currency, tailwinds or headwinds, and in the peer group whether it’s marked to model or marked to the last investment round. And I guess what we’ve proven in the past, Tilman, is on the way down and the way up, we’re very quick to change our valuation marks in line with our auditors, our PwC (our auditors). We have an audit committee inside every quarter. We sit down with them; we justify our valuations, and we wouldn’t put out a NAV if we didn’t believe in it.

So, our NAV. So, you’ve got our Q1 numbers coming and that will be a fresh NAV, and there will be some implications in that NAV, but those implications are more specific to what’s happened in Russia and Ukraine, because we’ve got a Russian asset, we’ve got exposure to the region and they will be impacted, i.e. you put a zero on them when you work your way back. It’s a small part of our portfolio and we’re very public in communicating that. But then, in other parts, we’ve seen some benefits of the ripple effects from the regional conflict, and I think Brazil is one of those positive ripple effects in what we’ve seen in the currency.

Dave Nangle, are down rounds ahead?

[00:28:13] Tilman Versch: Well, some investors also feared and brought questions looking at what Tiger Global did with the down rounds. Do you see any risk of this for you in a substantial way, or how do you observe these down rounds that are happening?

[00:28:30] Dave Nangle: It’s going to happen. I don’t mean it’s going to happen in our portfolio, but it’s going to happen across the board. I think what you’ve heard is you’ve had exuberant private markets for a very long period and all kinds of companies have benefited from that: weak companies, average companies, and great companies, and valuations have benefited from that. And now we’re going into a period where capital is, I don’t say totally risk-off, but more risk-off on both sides of the fence and we’re seeing that in later stage rounds already, and people are going to pay less for companies if they do pay.

We’re going to see companies failing. That’s going to happen. We’re going to see down rounds. Down rounds could be a good outcome for some companies versus failing. And then as always, we’re going to see the quality. It’s like buying a house: the quality house still gets the most bids and the premium pricing.

We’re going to see companies failing. That’s going to happen. We’re going to see down rounds. Down rounds could be a good outcome for some companies versus failing.

So, I think what’s key for us is that we think and believe we’ve paid the right price at the right time for these companies when we did pay them. They’ve been growing since, and mainly we’re heavy in Brazil, as we said, but also Mexico and India, which is a good kind of real estate in emerging markets right now, given all that’s going on. None of our big companies need to raise money this year, so they’re not going to get involved in markets. And we’ve raised a lot of money for Credit Us, Konfio, JUMO, TransferGo, Juspay – all our top five, six companies have all raised significant amounts of capital last year. Don’t need to touch these markets this year. And then we’ll see what happens as we roll into next year. And all will be growing at very healthy clips this year, given all we’ve seen so far.

So, as we stand here today, I’m very comfortable with our NAV. I don’t see the issues in our portfolio, but this is a crisis, Tilman, and these crises have legs, and they have ripple effects. So, you kind of size what happens in Russia, Ukraine, in the region then you get the ripple effects into macro, from food and commodity price, inflation, positives, and negatives.

Globally, we’re going to see a slowdown, all eyes on the US, what happens next on interest rate policy, and that ripples through everything else. So, very much, it’ll be a quarter-on-quarter NAV evolution and watching that space and there’ll be micro-level companies, as opposed to sweeping general statements. They know everybody needs to cut their NAVs or it’ll be like a specific company somewhere, then you get beneficiaries, you know, as well on the other side, we can’t negate the tailwind of the currency in Brazil.

We can’t negate the tailwind we’re seeing with Rupeek and gold prices in India, or with TransferGo, which is a remittance company for migrants in Europe. And all of a sudden, we’ve got the mother of all migrant moves in Europe because of what’s happened in Ukraine. So, I’m not talking about benefits from war, but it’s very clear their business is and will benefit. So, we’d be looking at everything on a micro-level but it’s defense-first at this point. You make sure everything is shored up, make sure everything is well funded, and then NAV then kicks in valuation.

Macro impacts on company valuations

[00:31:19] Tilman Versch: If you already get this topic, maybe try to take a look at the macro impacts on certain companies. You already told some stories. What other stories are interesting to hear for shareholders?

[00:31:31] Dave Nangle: Yeah. Look, everybody gets the macro playbook out and there are some great economists out there and there are some countries that are just built for these kinds of windows. They’ve got very strong balance sheets; they’re commodity or food producers and I guess we’re quite lucky to have over 50% or 60% of our NAV in Brazil. We just did two more deals in Brazil this year. So, we’re very heavy in Brazil and we didn’t do it for macro reasons, but obviously, the macro is helping them right now and helping us.

Then you look at places like Pakistan and Egypt. We’re in Pakistan and we’re not in Egypt and both of those countries have weak balance sheets. They’re going to see pressure on the current accounts, they’re going to see or need help from external parties be that the IMF or bigger wealthier nations. They’ll probably see their currency devalue to a certain degree and that puts pressure on those local countries, and it’ll keep capital away in big amounts for a period. So, you know, it’s a real country-by-country approach. I think Mexico is somewhere in between, I think India looks good geopolitically and has a stronger balance sheet than it ever had. So, I’m actually quite happy given where our portfolio is today.

And I guess if we look back five years ago, we were very heavy in Russia and that’s where you don’t want to belong today, and we’ve exited that. We made good money for investors, and we redeployed that capital into different geographies, but that’s a different story. But I’m quite comfortable from a macro geopolitical thesis of where our portfolio is placed.

Brazil

[00:32:56] Tilman Versch: Maybe you can tell us a bit more about the impacts you see in Brazil and why it is a positive for the country, the current situation?

[00:33:09] Dave Nangle: Yeah. Let’s not get too carried away. I’m not saying I’m living in a dreamland and Brazil is going to go to the moon while the world falls apart. There will be a global macro slowdown as a result of what’s happening. The ripple effects will happen everywhere. And we’ve seen inflation pick up even in Brazil and now interest rates are at double-digit levels. So, I see it on a micro-level through Creditas where it grew its loan book three times last year in 2021 – that’s public information. Will we grow 50% to a hundred percent this year? That’s more reasonable in an environment like this for a story like that. So, it’s not the year for everybody to go gung-ho on growth. It’s the year for a little bit more conservatism across the board while still seeing solid growth in most companies.

But I think Brazil, is food, it is commodities, oil, gas, et cetera. That’s obviously key for Brazil’s exports. That’s feeding true to a stronger currency as well as the high-interest rates in the interest rate trade versus the US. It’s a very nice tailwind when you’ve got assets in Brazil, which are a hundred percent Brazilian Real and you’re investing with hard currency. You don’t expect that, you’re not forecasting it. That’s not what you’re looking for from a micro-level company. You’re looking for them to compound and win their space and to exit. But if you get tailwinds along the way, especially when there’s a lot of stress in the world, you take it.

But I think Brazil, is food, it is commodities, oil, gas, et cetera. That’s obviously key for Brazil’s exports. That’s feeding true to a stronger currency as well as the high-interest rates in the interest rate trade versus the US.

Dave Nangle on capital allocation

[00:34:34] Tilman Versch: Interesting insight into Brazil. Do you play an instrument?

[00:34:44] Dave Nangle: I do not play an instrument. I would’ve tried guitar over the years, but I failed miserably. So, no, I don’t play music.

[00:34:51] Tilman Versch: Then maybe let’s do it with the keyboard picture or the keyboard metaphor. So, if over the last years – I think the last two years – you saw a bit more playing on the instrument set or the keyboard set of capital allocation and capital raises. And now with the bond, you made something. Maybe walk us a bit through what you think about capital location distance, capital raises also in this environment with the high discount to NAV?

[00:35:24] Dave Nangle: No, it’s fair. Look, over the seven years that we’ve been existing, we’ve done a little bit of everything in terms of the capital front. We started off with a rights issue and then we had an exit from a public company which is Tinkoff, we had an exit from a private company which was Iyzico. We’ve done two direct placements and now, we have issued a bond – our first bond – and a social bond for sustainable finance. So, a very key kind of marker on our ESG footing.

So, we’ve kind of stretched our wings in terms of how we attract capital into VEF and we’re very grateful for the various pockets of capital that have come our way. And we did a bond this time specifically because of what you said, Tilman, because of where our share price is trading. It’s trading at a deep discount to NAV, and it’s the window where you will be buying back your shares, not a window where you’d be issuing your shares. And we’re very aware of that, hence the bond.

Our framework was there for us, and the capital support was there, and we were low on capital after Q1. We ended 2021 with 62 million of cash capital and following investments, we were below 30 million at the end of Q1. So, we needed to replenish that capital and just be in a stronger capital position given what’s coming down, or what potentially is coming down the path in terms of either risks and headwinds, and you want to be able to support your companies or opportunities because of those risks and headwinds and new companies. And hence, we wanted to replenish. What I would say is we will probably raise more capital in the future and that’ll be a function of our share price, and would it be a rights issue, would it be a directed placement? We’ll see, and we’re very open to both.

We touched on Creditas earlier and I didn’t answer your question about IPO and exit. It’s still a company that wants to IPO. It will be IPO-ready this year, and they’re very clear in communicating that to the market. But will the markets be ready for them this year? Probably not. They’ll be more likely no than yes. So, it’s a 2023 playbook and that’s where we can see more capital potentially coming in where…it’s a name we’d like to keep for longer given everything we know about the company, but it’s also potential for us to take some capital off the table. And we’ll see when that journey comes around.

So, I think exits equity placements are still very much on the table. The bond gives us a nice breeding room and capital comfort. And then, there’s obviously the potential to buy back our stock, something we can’t do right now unfortunately because of our Swedish holding company and the fact that we’re listed on NASDAQ First North, which is a secondary exchange in Sweden. But the important thing for us and for our shareholders is we’re moving to the main board. So, we’ll be on the main Swedish stock exchange if everything goes according to plan in the next three to six months. There are lots of positives within that, but also within that, we’re allowed to buy back our stock again.

Listings

[00:38:11] Tilman Versch: What about the other positives that are coming from this re-listing?

[00:38:16] Dave Nangle: Well, A, we’re on an unregulated exchange. So, even though we act and operate like a regulated entity given our shareholder base and what we do, officially run an unregulated exchange and that keeps certain pockets of capital away from your share. You move to the main board; it means you’re open for all pockets of capital globally. We like that. It takes away some of the minimum thresholds people can hold in your stock because you’ll be regulated. And it also comes with more fund flows and more eyeballs from retail and tracker funds, et cetera. So, it just means effectively, you grow up as a company, you’re on the main board and you’ve access to all areas for capital as opposed to certain areas.

Cash

[00:38:56] Tilman Versch: You already mentioned cash. So, maybe, what do you think about cash inside of VEF? Is it something you want to hold to a certain extent to be able to be aggressive and volatile faces, or is it like Dave has this telephone in his hand, and he’s always able to call some of the core shareholders and say, maybe, “we need you to wire a bond or a capital raise to give us cash to be more aggressive in these phases”? How’s it going there with cash?

[00:39:25] Dave Nangle: The magic phone. Make some calls, get some capital. Look, it’s a balance. So, we would like to be light on capital and then just call capital as in when we need it i.e., by equity or via debt. But the reality of the situation is you are a slave somewhat to markets, and when markets are poor like they are now, your share price trades down as it does. And it’s more difficult because your shareholders are also having difficult times and they’re seeing lots of opportunities to deploy capital, or maybe they’re playing defense as well.

It’s a bit perverse when times are good and everything’s fully valued. There’s more capital on the table to play with. So, I guess the way we think about it is we like to keep enough capital to be strategically flexible in what we do, but not too much capital that we’re going to hurt overall performance, but there’s a bit of giving and take in that tussle. I think we got too low on capital in Q1. I think now after the bond sitting on 70 to 80 million of capital or cash capital, and about 10% of our NAV, it’s a good place to be both for downside protection, upside flexibility, and not too much drag on performance. So, I’d kind of like to keep it give or take in the five to 10%. Closer to 10% would be comfortable from my side.

So, I guess the way we think about it is we like to keep enough capital to be strategically flexible in what we do, but not too much capital that we’re going to hurt overall performance, but there’s a bit of giving and take in that tussle.

Insight into two portfolio holdings: Creditas and Konfio

[00:40:37] Tilman Versch: That’s an interesting insight. Let us move on a bit and look at your core portfolio holdings, and I want to focus a bit on Creditas and Konfio. Maybe you can walk us a bit through the investment thesis behind these companies, what value do the companies add to the customers, and why are they growing so strong?

[00:40:59] Dave Nangle: Okay. Let’s start with Creditas, our baby. It is over half of our NAV. And if you want to know about VEF, you want to know about Creditas, and if you like it, you go a long way to liking us. And it is a special and unique company in that what they do in Brazil, which is a scale market, are they provides secured consumer lending. So, Brazil is a very large consumer loan market. It’s about a 500-billion-dollar existing loan market today. So, it’s not like it’s one of these emerging markets with future potential growth that actually exists. The problem is, a lot of that lending is unsecured lending: it’s a credit card, it’s an overdraft, it’s personal loans. So, it’s a high rate, short-duration loan to individuals in Brazil where a lot of these rates can be as high as triple-digit annual or double-digit monthly rates.

And it [Creditas] is a special and unique company in that what they do in Brazil, which is a scale market, is they provide secured consumer lending.

What Creditas then does is it provides a better product market fit, it’s providing a secured product secured against your home or your car or your payroll. And once there’s security or collateral against it, they can charge you a lower rate than the banks do on average, and better duration. You can get a longer duration loan, more fit for purpose. So, I think it started with that.

It’s not that banks can’t do this product, or don’t do this product. They just don’t push this product because their core unsecured loans are much more monetizable, and have better unit economics for the banks. So, Creditas pushed this product – and it’s a product that exists in Western Europe, in the US and it’s very deep and rich – but they were kind of pioneers of it in the Brazilian market, and they’ve been doing it for over 10 years now. Because of the size of the addressable market, they’ve just been compounding from a 50 million loan book to a hundred to 200. As of today, it’s an 800 million loan book. So, this is as of year-end at ‘21, and this is public information.

Because of the size of the addressable market, they’ve just been compounding from a 50 million loan book to a hundred to 200. As of today, it’s an 800 million loan book.

And the way they’ve built this business is they fund it all off-balance sheet. So, it’s an off-balance-sheet funded model, locally, all local currency, all matched into a scale market with a great product-market fit with supernatural unit economics, and they’ve proven they can scale the team, scale the products, scale the volumes. And in what’s happened then over the last 12 to 18 months, as they’ve gone through each of those ecosystems: home, auto, and payroll or work, they started to roll out more products, whether it’s insurance in payroll into benefits and I’d also say insurance, but also auto i-buyer. So, you’re getting different product suites into that core relationship and doing partnerships with some of the big entities in the FinTech scene in Brazil like Nubank as they cross all their products into their client base.

So, it’s been a very exciting journey where they’re really delivering on a scale opportunity, which is the core. That’s got lots of room to compound and going back to my earlier point, you can forecast the compounding nature of that as they have the capital, the funding, the product, the product market fits and they’re just improving incrementally as they go. And it’s a very strong team. And then they’re expanding, broadening, and deepening the TAM as they go. The more time we spend on Creditas, the more we like it hence we’ve given them more and more capital over four rounds from series C when we first invested back in 2017 right up to their series F which was done in Q4 last year.

It’s very hard to find a story like Creditas, like a Tinkoff for us in the past, or an Iyzico. And when you do find them, you get closer to them. You sit on the board, you see what’s happening, you have an inside track, you just get as much capital as possible and enjoy the ride.

[00:44:23] Tilman Versch: And maybe you can also explain a bit more on Konfio, like, what value do they add for the customers? Why could they grow so strongly?

[00:44:32] Dave Nangle: It’s fair. It’s Mexico versus Brazilian stories talked about, but still a scale market. There are 130 million people, but where does Konfio focus? It focuses on small businesses versus credit costs on the consumer side. And what you’ve got in Mexico and why we like the small business space in Mexico is because there are 7 million small businesses in Mexico and the banks just don’t service them. So, this is more about financial inclusion and under penetration than the banks treating them badly or having too high prices.

So, if you are a big corporate in Mexico or a rich or a middle-income individual, the banks will take care of you. So, it’s very good banking for the top end. Then, at the very bottom end, there’s kind of microfinance or do-gooder institutions. So, there’s a lot of folks on that, but in the middle, small businesses, and you obviously tell me you’re from Germany, which is a home of the small business, there’s just no small business banking going on. And we’re talking credit, for one, we’re talking payments, we’re talking software for management information systems, we’re talking just basic banking products.

So, Konfio started, once again like Creditas, maybe 10 years ago, focusing on credit – working capital for small businesses. It built out that product. It was rolling, it’s scaling, it’s still scaling it today. And then it moved to product number two which was ERP, you know, zero models, or into a QuickBooks for small businesses. Then the third product, they made an acquisition last year in payments like merchant acquiring, like the Square Model in the US or Zettel or SumUp in Europe. And now, it’s applying for a banking license. So effectively, it’ll be a digital bank with a full suite of services for the Mexican small business. And that’s what they’ve been building.

So, Konfio started, once again like Creditas, maybe 10 years ago, focusing on credit – working capital for small businesses.

The interesting thing is we’re shareholders in Konfio with much of the same shareholders we are in Creditas. The two founders know each other very well, so there’s a lot of kind of cross-pollination and ideas sharing in those two markets and those two businesses. I’d say Konfio is probably running about 18 months behind Creditas, not a negative, but just in terms of size and shape and stage of its journey. Whereas Creditas is IPO-ready or thereabouts, Konfio’s a little bit behind just given us traction and this type of journey versus what Creditas is.

Community exclusive: Expectations for the cooperation between Creditas and Nubank

[00:46:44] Tilman Versch: Very interesting. Let’s do some more deep dive on Creditas. So, what can shareholders expect from the cooperation with Nubank that was recently announced, and maybe you can also explain what Nubank does, for people who don’t know Nubank, in Brazil?

[00:47:01] Tilman Versch: Hey, Tilman here. I’m sure. I’m sure you’re curious about the answer to this question, but this answer is exclusive to the members of my community, Good Investing Plus.

Good Investing Plus is a place where we help each other to get better as investors day by day. If you are an ambitious, long-term-oriented investor that likes to share, please apply for Good Investing Plus. Just go to good-investing.net/plus. You can also find this link in the show notes. I’m waiting for your application. And without further ado, let’s go back to the conversation.

Without further ado, let’s go back to the conversation.

Creditas’ loss

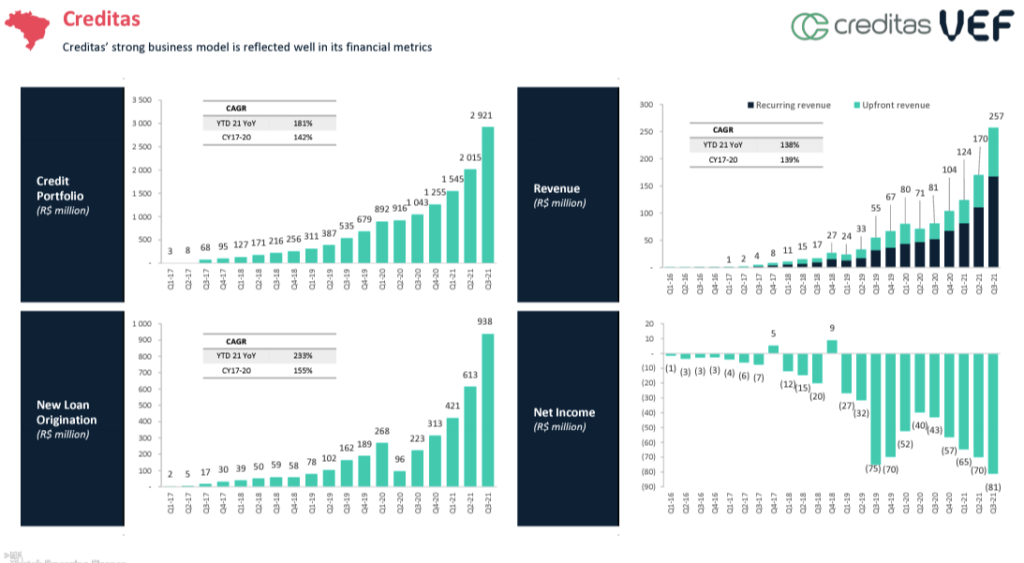

[00:47:41] Tilman Versch: In your presentation, you disclosed some key metrics for Creditas. Maybe let’s take a look at them, and maybe help me to understand the revenue side and the net income side of Creditas? Maybe let’s begin with the dummy question. Why is the net income for Creditas, like, the loss is growing year over year, over year, and how should I understand this loss? It’s a dummy question, but yeah.

[00:48:08] Dave Nangle: No, you don’t want to extrapolate that. Look, you got a company in fast-growth mode, and in the top-right chart is the revenue, and this is all public information. So, this is their quarterly revenue, and this is all in local currency. So, this is Brazilian Real divided by five, give or take, to get your dollars. So, it’s a company that’s very much growing on the origination side, on the left-hand side, and on the revenue side. Its unit economics are strong, such that on a contribution margin level, they’re profitable, and where they break even before effectively customer acquisition and expansion. So, where those losses have been racked up is effectively a function of them aggressively expanding. There’s been a whole new raft of M&A and expanding into new countries like Mexico, and mainly, it’s the customer acquisition spend where they’re spending incremental dollars to bring customers through the door.

So, where those losses have been racked up is effectively a function of them aggressively expanding.

Now, every customer at Creditas is a paying customer. So, once they come through the door and they spend money to acquire that customer, that customer becomes a one-year, two-year, five-year customer on a revenue product, on a secured loan.

What we’ve done in the past, and you see kind of blips of positivity in that kind of negative chart for net income, is where they stopped. They say, “Let’s stop acquiring.” And what it shows is the core business is profitable and that’s…this is all spending for future growth. And what you’re going to see starting to happen through 2022 is that that chart starts to tear up, and because we’re moving towards IPO, the growth will be less; the machine is scaled now as to say 800 million in Q4 of the loan book, which is paying and there are fees being paid on top of that.

So, you’re going to start to see the trend going back up into the right towards that kind of breakeven point because the markets want, and they should want, a company that’s not only strong, growing with a big addressable market, but also one which is a path towards profitability from here. And Creditas, at its core, is unit economic positive, but it’s that expansion, and that’s kind of customer acquisition, which is a region for the burn.

Creditas’ efficiency in customer acquisition

[00:50:12] Tilman Versch: What are the key costs in this customer acquisition? Like, where does Creditas spend the money towards, and how efficient are they in your eyes?

[00:50:24] Dave Nangle: The good thing is they’re getting more and more efficient. So, the direction of travel on customer acquisition is improving, quarter on quarter almost for the last, I don’t know, 12, 16 quarters. It just continues to trend down in terms of what they pay for a customer.

I won’t get too much into the specifics of the numbers, but, if they’re lending a hundred dollars, they will be taking 30% on average of that as interest income and over 1, 2, 3, 5 years. So, 30% a year off the top of that, what they pay upfront to acquire that customer can be 10%, can be 20% of that loan value. So, up front is a very meaty amount of customer acquisition cost to pay, but then over the life of the loan, you more than get that back in the return, and the capital return is very high. Hence, the upfront customer acquisition costs are quite high, but they’re getting more and more efficient as they grow.

So, up front is a very meaty amount of customer acquisition cost to pay, but then over the life of the loan, you more than get that back in the return, and the capital return is very high.

[00:51:20] Tilman Versch: And how do they make sure that the loan doesn’t default over time? And like they have the right customer?

[00:51:30] Dave Nangle: They have the right customers, A, and B, they have the right collateral. I think B is more important than A, and that’s the beauty of collateral lending because if I lend to you, Tilman, and I give you $10,000 and I hope you pay me back cause I score you because of your good credit history…but if I give you $10,000 and you collateralize it against your home, which is worth $500,000, and if you don’t pay me, I can take your house. It’s very likely you’ll pay me. So, the collateral is important.

They [Creditas] have the right customers, A, and B, they have the right collateral.

Recurring and upfront revenue

[00:52:03] Tilman Versch: Okay. And maybe another dummy question, if you could look at the recurring revenue and upfront revenue chart above the net income, can you explain the term recurring in this sense and upfront?

[00:52:20] Dave Nangle: Yeah. Like there are fees and it’s interest income for Creditas, especially on the credit products. So, the upfront fees that they get off customers for underwriting the loan are upfront, and also the funding structures that they fund off-balance sheet, they actually get paid for sourcing the loan and securitizing them. So, there are a lot of fees that come up front. And then there is the life of the loan where they’re getting interest income over the 1, 2, 3, 5-year period. So, it’s that mix.

But what I would say, is this is all a Brazilian gap in local accounting standards. Not to get too boring, we’ll move to IFRS and there’ll be different accounting treatments of all these things, and we’re going to evolve that way as we move towards IPO. But I guess the way IFRS goes is you get more conservative at most things. You take provisions upfront, you can take fees over the life of the loan and so, it’ll all be morphed and merged a bit as we go.

Dave Nangle on rethinking sizing

[00:53:07] Tilman Versch: This episode is also a bit about fears of investors, and you already mentioned Tinkoff in our conversation. This was once your largest holding, I think, and if you look at the share price of Tinkoff, which is a great company, they went from 90 to three dollars at the moment due to the Russian invasion. And if you think about, like, the willingness in the emerging markets to underwrite, like the huge concentration you have with Creditas, is this what you’ve observed now with Tinkoff? A bit challenging your mind there, and let you rethink sizing about a certain threshold?

[00:53:52] Dave Nangle: Simple answer – no. We’re not reckless with investor capital, but we’re not calling global geopolitics. That’s not our mandate. Russia is special in that regard. Russia has a tendency to go to zero every so often in some way. I’ve seen it so many times, so many crises in Russia. This one is different. They’re all different, but this one has a darker edge to it, and we all know that and are very aware of it, and the ethics are pretty negative there. But Tinkoff is a phenomenal asset and a phenomenal business, arguably one of the best, if not the best, digital banker FinTech in emerging markets. Nothing that Russia’s done has changed that fact. It was built by an entrepreneur – not an oligarch – built from scratch with a very strong team, loyal, hardworking, and skilled who have been with them through the journey, revenue first, unit economic first, profitable first.

Russia has a tendency to go to zero every so often in some way. I’ve seen it so many times, so many crises in Russia. This one is different.

Nothing’s perfect, but they are as close to perfect as you get in the EM FinTech world. And what’s happened to them is a function obviously of what’s happened on the warfront and with Putin and the invasion in Ukraine. And you said, it’s trading at $3 a share, but it’s trading at $3 a share and not trading. So, it might as well be worth nothing albeit it is very much a going concern. So, what does that say to me? These things can happen, of course, they can. They’re more likely to happen in certain emerging markets i.e., Russia than in others.

We don’t mind concentration, though. I’m very happy with our Creditas concentration for all the reasons that I said, but there will be a time when we’ll be out of that and something else will be concentrated in. We were heavy in Russia in the past and we’re heavy in Turkey today, we’re heavy in Brazil, we’re looking at India, three investments and growth, and we’re looking at doing our first investment in Indonesia. So, we keep on evolving as we go and as we grow.

But yes, we have to be very aware of what happened in Russia, and we did a lot of souls searching after we exited Tinkoff effectively at $70 a share and watched it go to, as you said, a hundred dollars and we asked ourselves, you know, “Did we miss a trick?” We knew the company well, arguably best, we were on the inside, it was compounding, and we left a lot of money on the table. But now it’s worth noting, and we look clever. So, yeah, the truth’s somewhere in between.

We knew the company [Tinkoff] well, arguably best, we were on the inside, it was compounding, and we left a lot of money on the table. But now it’s worth noting, and we look clever.

Learnings from the Russian conflict

[00:56:13] Tilman Versch: Are there any other lessons you’ve taken or learnings you’ve taken from this impact of the Russian invasion of Ukraine and what has happened there for your investment style and your approach? You have some impact in the portfolio, you can also explain to them if you want, but it’s more about the lessons and if you’ve changed anything in your process of thinking.

[00:56:36] Dave Nangle: Yeah. To be honest, no. And that’s not saying we know everything or we’re not learning, we’re learning lots, always. I’ve been around a lot of Russian and Russian-related crises in my life and it’s the first time it’s happening, and I’m not brutally exposed to it. So, we have a very small exposure.

Revo, a buy-now-pay-later company in Russia, is a very good company growing and is profitable, but it lives in a parallel universe right now and we’ll see where that universe goes. We were very able to size, and shape our exposure to the region, very able to look through to the global aspects and ripple effects of that. But now, lesson-wise, I don’t think we’re looking at this and taking anything away. If anything, we’re questioning, “Can we invest in Russia again?” That’s a question, ethically, fundamentally. I think we sit on that one for a while because obviously with our structure, our long duration, arguably there is an opportunity for us to put capital to work in Russia and maybe, maybe not. And these are questions that we’re asking ourselves and asking our investment committee and talking with our shareholders. So, these are things we’re thinking about, but I don’t think we’ve taken any real hard lessons from this so far and looked to change anything that we do.

But now, lesson wise, I don’t think we’re looking at this and taking anything away. If anything, we’re questioning, “Can we invest in Russia again?”

Konfio’s future

[00:57:57] Tilman Versch: Let’s go back to Konfio, and in your annual report, you have written a quite interesting sentence: “Konfio now has all the pieces of the puzzle in place to grow into a multi-billion-dollar company”. So, why is that?

[00:58:14] Dave Nangle: First of all, it’s easier said than done. Second, you can have all the pieces in play you still need to execute. But why is that? I think it’s a function of when we invested in Konfio, it was a monoline; it was a single product company focusing on working capital for small businesses. And their promise to us when we did invest was that they would keep on focusing on that while adding in more product suites. And they have added in the payments, they added in the ERP, and they’ve added in, hopefully soon, a fully digital banking license for the company. And that means it can be the number one small business financial ecosystem in Mexico because it can offer everything to small businesses in financial services.

And their [Konfio] promise to us [VEF] when we did invest was that they would keep on focusing on that while adding in more product suite…and they have…that means it [Konfio] can be the number one small business financial ecosystem in Mexico because they can offer everything to the small business in financial services.

Now, the key for them is execution. They need to take the sum of the parts and put them together and make it a valuable whole. That’s where we sit around as a board and as a management team, and they look to bring all those products together when they’re talking to small businesses so they can offer the full offering. So, that’s why it gets very exciting, but this is where the work is done. Everybody likes to talk about acquisitions and raising capital, but sometimes, your companies need to put their head down and really deliver, and that’s the point where we are in with Konfio right now.

Interesting learnings

[00:59:27] Tilman Versch: Looking at these two companies, but also the other portfolio companies you invested in, is there anything that has surprised you over the last year, or are there any super interesting learnings you want to share with us?

[00:59:43] Dave Nangle: Like, there’s always learning. So, we keep on learning. But specifics, I guess the importance of strong founders is always key. As much as companies and numbers, we talk about being analysts, founders make things happen. They make capital come through the door; they make good hires. So, we keep on seeing that with some of our founders where they keep on impressing us on that front, and that’s a key. So, the founder first, founder centric – get the right founders then start thinking about everything else. That’s always the way.

As much as companies and numbers, we talk about being analysts, founders make things happen.

I think we talked about it earlier, it’s just not getting caught up in the euphoria of markets and pricing because, as always, it turns, and it’s turning again, and it’ll turn again, and we’ll get into a new cycle of fun. I’m not saying we’re the cleverest kids in the street, and we knew this would happen. We were putting capital to work last year, but we think we put it to use those good valuations, but, you know, it’s there.

And I guess the last thing, we’ve got some great investors, and it’s just great sitting down with the Fidelities and the Wellingtons and guys at Roon, kind of who are one of our biggest shareholders. And you know, you talked about our share price falling and different negative aspects of any cycle like this, but this too shall pass. It always does. And you got to be sitting there on the other side of this. So, you need to play defense first, you make sure you’re strong, you’re positioned and then you start thinking about the opportunities, hence we raise money via the bond, putting more capital to work so that in 12 months or 24 months or three years’ time, you look very good and clever about what you did in this window, as opposed to sitting back and worrying about your share price in the short term.

Dave Nangle on the next Creditas?

[01:01:30] Tilman Versch: So, a quite easy question on your portfolio: what will be the next Creditas in your portfolio?

[01:01:38] Dave Nangle: The next Creditas. Look, we talked about Konfio already, but I think one to watch if you’re a shareholder in VEF, is JustPay in India just because it’s a phenomenal company. It really is a very strong engineering product-first team, they got a great product-market fit with what they do on the payment space on mobile: mobile-first, mobile-only, the partners that they have and that they’re attracting from a customer point of view from the Ubers, the Amazons, the Olas, they’re letting their technology inside their app. And they’re compounding with these companies and doubling year on year and also rolling out new products which are higher unit economics. So, we’ve got a team on the ground this week in India with them sitting down, catching up, and everything. If I was a VEF shareholder, obviously do your work on Creditas and Konfio: that’s where the juice is today, but next-gen is JustPay.

If I was a VEF shareholder, obviously do your work on Creditas and Konfio: that’s where the juice is today, but next gen is JustPay.

The next Konfio?

[01:02:38] Tilman Versch: And who will be your next Konfio?

[01:02:45] Dave Nangle: You could probably go down to the earlier ones and the younger companies and-

[01:02:50] Tilman Versch: Or which companies are you, like, where you say, “That makes me bullish?” Like, it’s hard to say…it’s you have 15 kids and you love all your 15 kids, but this kid has such a great talent?

[01:03:03] Dave Nangle: No, I know. I’ve got three kids and I’ve got favorites all the time and I’m not ashamed to say it. But with our newer investments, it’s hard to get away from the new ones. So, you know, AB, I’m wearing AB’s t-shirt here. I just back from Pakistan, energized after spending a week in Pakistan with them. And they are a phenomenal company in the financial wellness space with a great founder and will raise more capital and will compound a lot of value for us as shareholders. So, I really like that one.

And then we did a deal in Brazil with a Q1 company called Gringo. It’s a car app growing like a weed: great customer market or product-market fit there, great unit economics, and how they process payments for all aspects of a driver’s needs in Brazil, be that fine, registration certification. It’s kind of a hidden niche on a scale niche at that.

I’ve got a couple of other interesting deals coming down the pipe so, you can’t help but get excited too much about the new ones, it happens. But as an investor, I’d say focus on Creditas, Konfio, and JustPay and then let the rest kind of season a bit and they’ll come true nicely.

But as an investor, I’d say focus on Creditas, Konfio and JustPay and then let the rest kind of season a bit and they’ll come true nicely.

Egypt

[01:04:11] Tilman Versch: A market where you’re just laying the groundwork, I think you haven’t announced any deals. And you said in your report that you like what you see coming out of Egypt a lot. What could you observe on the ground and why did you like it?

[01:04:29] Dave Nangle: It’s, I hate to say, like a hundred million people, and you kind of hear people saying in Pakistan, 200 million people. It’s a very simplistic terminology, but it is a scale African or Middle East market. We like single-country plays because that’s where you get the most juice; when companies cross borders, they can get more and more difficult. They have a nice tailwind from a regulatory point of view and government point of view, digitization. So, the direction of travel seems to be somewhat akin to what we’ve seen in markets like India or Brazil, albeit at an earlier stage.

So, the direction of travel seems to be somewhat akin to what we’ve seen in markets like India or Brazil, albeit at an earlier stage.

And we’re getting a local ecosystem of venture capital funds, seeding companies for seed, and series A. So, we’re starting to get the ecosystem, the capital, the regulation, the governance, and obviously, the population is hungry for this. So, that all feed well. I think what’s less well is just, you know, unlike Pakistan where we’ve done two investments, about to do three, and we haven’t yet found the company or the founder we want to back yet. That can change very quickly, but it’s a function of finding that before we put capital to work more than anything else. So, I’d say we are open and happy to invest in Egypt. We just need to find the right opportunity.

Playbook to open new markets

[01:05:42] Tilman Versch: What is your playbook to open such a market for you, if there’s any playbook?

[01:05:48] Dave Nanle: No, there is a bit of a playbook and people ask us how we can sit here in Europe and do what we do, but it doesn’t take a lot…

[01:05:55] Tilman Versch: There’s this internet, there’s this internet…

[01:05:59] Dave Nangle: It is this internet. But we’ve got a reputation and a brand for EM and FinTech. We’ve got relationships across the globe in the VC world. We travel, we hit the ground, and we learn the public side from the government, from the macro to the politics to the listed companies, the banks, and the telcos.

We travel, we hit the ground, we learn the public side from the government, from the macro to the politics to the listed companies, the banks, the telcos.

In Egypt, there’s a company called Fawry which is a kind of FinTech 1.0. You get inside that, you travel on the ground, you meet the local VCs, you meet the entrepreneurs. And because there are so few people doing this, like us, it doesn’t take a lot to become the global expert in Egyptian FinTech. And that the competition is very small because not a lot of people are dedicating a lot of resources or time to that other than the locals or the regional guys. And then you become one of five, one of 10 people looking in-depth at that market, having a resource with their finger on the pulse, looking at that. And then you find the founders that you like and the spaces that you like, and you drill, and you dig, and you dig and then opportunities arise, and you try and take them.

Climate risks

[01:06:57] Tilman Versch: Very interesting. In the end, I want to talk a bit about climate risks because you tend to concentrate on countries that are close to the equator, where you already have a lot of heat and humidity, and you see the impacts of climate change more strongly in my eyes. How are you thinking about climate risks with the investment process you’re doing?

[01:07:20] Dave Nangle: Yeah. I don’t get asked that question every day, to be honest. From an ESG point of view, not that we’re ignorant on E and obviously G is a given listed entity in Sweden. We focus a lot on S and sustainable finance and financial inclusion and wellness. So, that’s kind of in our strength and hence the bond that we raised.

From an environmental point of view, obviously, there are individual thoughts on that, but from an investor point of view, we’re not exactly investing in that albeit we do have a very interesting deal done in the making that was announced in our annual report. We haven’t formally made a lot of noise about it where we’re going to invest in a solar company that lends against solar panels just because of the climate aspects of Brazil specifically, and the opportunity in that space and the credit behind rolling out that product.

So, I’m not saying, Tilman, we’re ignorant of it. I wouldn’t say we’re overly focused. This is throwing up some opportunities and we need to take advantage of them, and we need to have a strong ESG playbook and watch our aspect of that. But no, I haven’t seen it come to the floor as issue number one in the countries that we focus on.

[01:08:35] Tilman Versch: Do you fear any impacts of climate risk at a certain point on your portfolio that certain regions will have problems accessing capital markets, migration as a topic?